As living expenses rise and wages stagnate, many families are opening their homes to aging parents, especially if their parents are disabled and unable to afford long-term care.

Multi-generational households are a norm in many cultures, not only for affordability but for the village it takes to raise children and build community. But it’s not the norm in the United States, where we prioritize independence and rugged individualism.

If you’re able to open your home to your parents and take on the costs of supporting them in their later years, that’s a wonderful thing to offer. If you can’t afford to help, our last blog post can help with suggestions to reduce costs for them to make their dollars stretch.

For this post, we’ll assume that you have the space, the means, and the wherewithal to support your family’s elders, and we’ll explore the potential tax impacts of doing so.

Claiming a Parent as a Qualified Dependent

If you provide over half of your parents’ support during the year (including living expenses, medical costs, really anything that they need to live), you may be eligible to claim them as a qualified dependent on your tax return–but only if they meet certain requirements.

Test 1: Not a qualifying child: Pretty self explanatory, this first test means that the dependent you want to claim is not your own child who would qualify as a dependent.

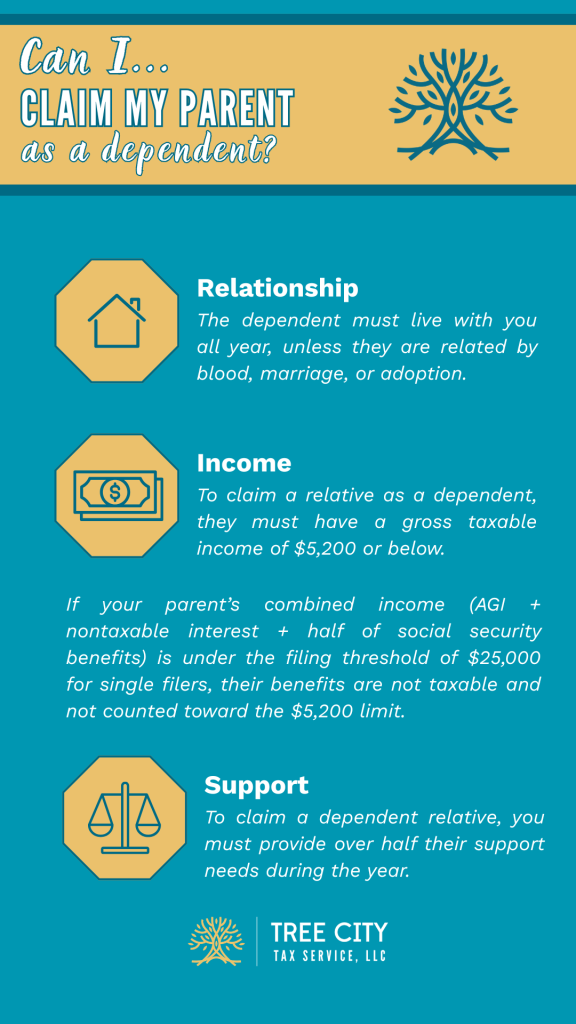

Test 2: Member of household or relationship – The dependent must live with you all year, unless they are related by blood, marriage, or adoption.

Test 3: Gross Income – To claim a relative as a dependent, they must have a gross taxable income of $5,200 or below. This is where most people will find that their parent or relative doesn’t qualify as a dependent.

What about social security income? If your parent’s combined income (AGI + nontaxable interest + half of social security benefits) is under the filing threshold of $25,000 for single filers, their benefits are not taxable. Tax-exempt income is not counted toward the $5,200 limit, so your parent may still qualify as a dependent on your return.

If you’re itemizing your deductions, you may still be able to get a tax break for medical expenses you cover for your parent even if they weren’t a qualified dependent. We’ll cover this under the deductions and credits section.

Test 4: Support – To claim a dependent relative, you must provide over half their support needs during the year.

See this example from the IRS publication 501:

A married couple lives with their two children and one of their parents. Their parent gets social security benefits of $2,400, which the parent spends for clothing, transportation, and recreation. The parent has no other income. The married couple’s total food expense for the household is $5,200. They pay the parent’s medical and drug expenses of $1,200. The fair rental value of the lodging provided for the parent is $1,800 a year, based on the cost of similar rooming facilities. Figure the parent’s total support as follows.

Fair rental value of lodging $1,800

Clothing, transportation, recreation $2,400

Medical expenses $1,200

Share of food (1/5 of $5,200) $1,040

Total support $6,440

The support the married couple provides ($1,800 lodging + $1,200 medical expenses + $1,040 food = $4,040) is more than half of the parent’s $6,440 total support.

If your parent passes all these tests and qualifies as a dependent, they cannot file a joint return.

If you share care costs with other siblings or relatives, one person can choose to claim the parents as dependents as long as they provide at least 10% of the support costs. All contributors to the dependents’ support costs must sign off on form 2120. Only one person can claim the dependent per year, but it does not have to be the same person every year.

Tax Breaks for Elder Care

Let’s assume your parent or step-parent meets the requirements listed above and they are a qualifying dependent you claim on your tax return. How can you maximize the tax breaks available for this situation?

Itemized Medical Expenses: If your household’s out-of-pocket medical expenses exceed 7.5% of your adjusted gross income (AGI), you can itemize your deductions and claim these expenses. This includes medical mileage to compensate for travel expenses to get to medical appointments.

It’s worth itemizing if you can deduct more than the standard deduction’s value ($15,750 in 2025, or $16,100 in 2026 for single filers).

Most importantly, you can itemize medical costs even if your parent made too much gross income to qualify as your dependent!

Specifically, the IRS says: You can include medical expenses you paid for an individual that would have been your dependent except that:

- He or she received gross income of $5,200 or more in 2025,

- He or she filed a joint return for the year, or

- You are properly claimed as a dependent on someone else’s return.

Dependent Care Credit: If you pay for care for your qualified dependent while you work, and they are unable to care for themselves, you may be eligible for the Dependent Care Credit. You can claim 20-35% of care expenses (the percentage depends on your income) up to $3,000 for one dependent or $6,000 for two or more.

Tax Credit for Other Dependents: You can receive a $500 credit per qualified dependent with this credit, which is an alternative to the Child Tax Credit for dependents who are not your children.

Head of Household: If you are unmarried and would normally file single, but you cover more than 50% of a qualified dependent’s support needs, you can file as Head of Household for a larger standard deduction. For the 2025 tax year, the standard deduction was $15,750 for single filers and $23,625 for HoH filers. That’s an extra $7,875!

Other questions?

If you have any other questions about claiming your aging parent or other relative as a dependent, please let us know! You can submit a question using our contact form or email us at info@treecitytax.com.